Freight is one of the largest operating costs in distribution businesses and often represents 5–8% of revenue. For a distributor generating $500M in sales, that can translate to $25–40M in annual delivery cost. In an industry where operating margins are often measured in single digits, freight and delivery costs can materially affect profitability.

Delivery behavior varies widely across customers. Order size, shipment frequency, and route density all influence the real economics of service. As a result, customers appear profitable on the top line may generate very different operating contribution once delivery economics more closely examined.

Freight cost-to-serve analytics brings operational drivers into profitability models so organizations can see the real economics of serving customers. By connecting delivery behavior to financial outcomes, companies can evaluate margins with greater confidence and identify where freight creates a hidden margin tax.

Get the Executive Brief

This executive brief, “Cost-to-Serve Analytics: Freight is the Hidden Margin Tax”, explores the challenge with freight cost-to-serve analytics and how finance teams are beginning to model freight and delivery economics more accurately.

What You’ll Learn

The executive brief highlights several economic patterns finance leaders are encountering as freight volatility and delivery complexity increase. It explores why freight is becoming a critical factor in distribution profitability, including:

- Why blended freight allocations distort customer profitability

- Where margin erosion typically appears in distribution P&Ls

- How delivery behavior shapes cost-to-serve

- Why freight volatility is structural, not temporary

- How finance teams can stress-test margin assumptions

Who This Brief is For

We created this executive brief for leaders responsible for understanding profitability in distribution businesses, particularly those evaluating how operational behavior affects margin performance.

It is most relevant for CFOs, finance leaders, profitability and costing professionals, and private equity operating partners who need clearer visibility into customer contribution and cost-to-serve economics.

A Common Profitability Illusion in Distribution

One of the patterns highlighted in the executive brief, “Cost-to-Serve Analytics: Freight is the Hidden Margin Tax”, is how freight allocation can create a misleading view of customer profitability. When companies blend delivery costs across customers or shipments, margin reports often suggest similar contribution across customers. In reality, differences in delivery behavior, such as shipment size, order frequency, and route density, can materially change the economics of serving each customer.

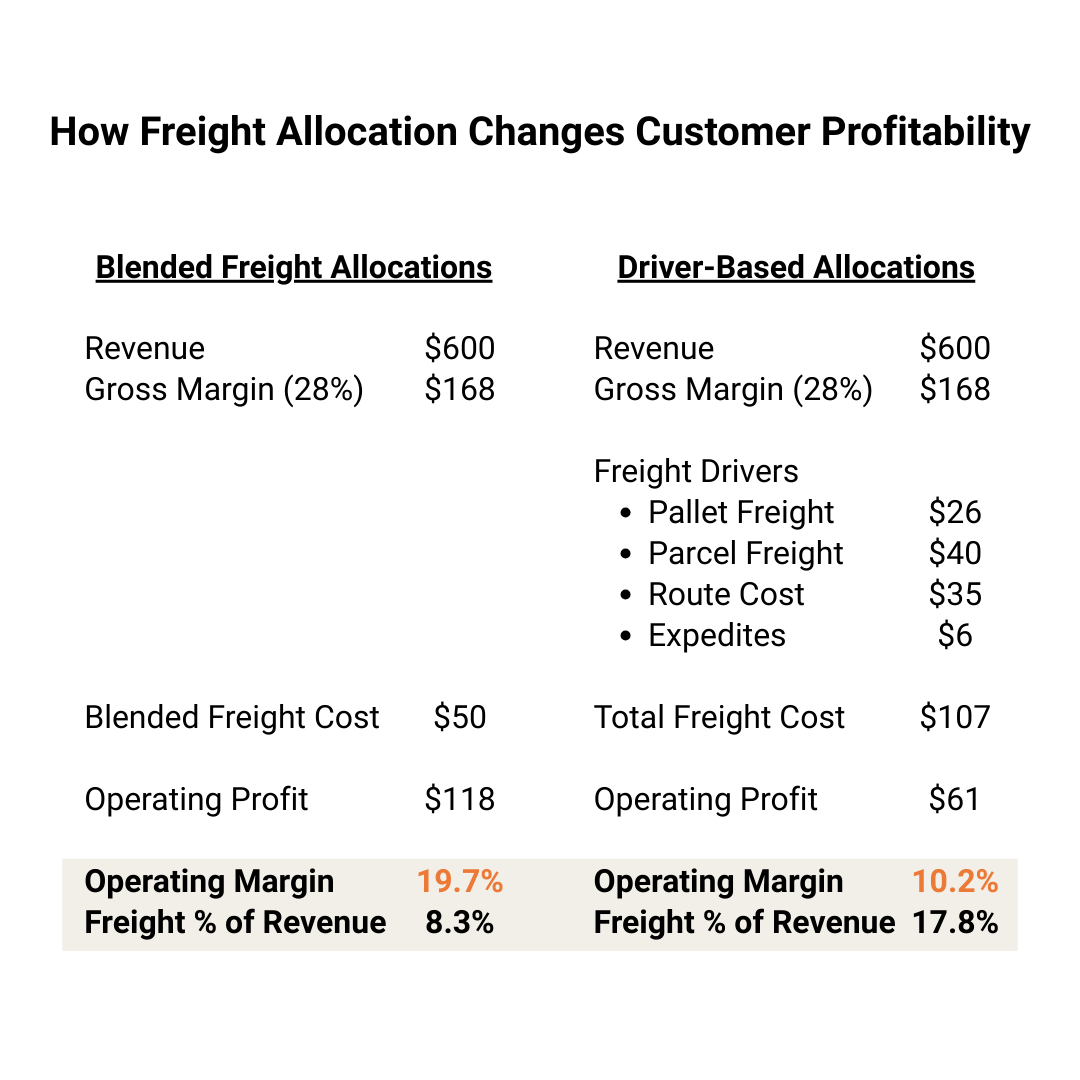

Customer Profitability Comparison

This example from the executive brief illustrates how freight allocation methods can change the apparent profitability of the same customer.

Under a blended freight allocation, companies spread delivery costs broadly across revenue. The customer appears highly profitable, with a strong operating margin.

When organizations model freight using operational cost drivers such as shipment type, routing, and expedites, the economics look very different. The driver-based view captures the full delivery cost required to serve the customer.

This difference illustrates one of the central themes of the executive brief: how traditional freight allocations can mask the true cost-to-serve and distort customer profitability analysis.

Three Economic Shifts Reshaping Distribution Margins

The executive brief highlights several shifts in delivery economics that are beginning to reshape profitability across distribution businesses. As freight volatility increases and customer ordering behavior evolves, finance teams are discovering new patterns in how margin is created and where it quietly erodes.

Freight Is Becoming a Margin Variable

Freight has traditionally been treated as a logistics cost. But as delivery patterns fragment and service expectations evolve, it increasingly shapes the economics of customer profitability. Small differences in order behavior can create meaningful differences in contribution.

Margin Distortion Often Appears After Gross Profit

Many organizations focus heavily on product margin. Yet in distribution businesses, delivery cost, service complexity, and handling often reshape profitability between gross profit and operating profit. This is where meaningful differences between customers often emerge.

Allocation Methods Can Hide Economic Reality

When freight is allocated broadly across revenue or shipments, the margin model can mask meaningful differences in customer contribution. Over time, those distortions influence pricing, service policies, and growth decisions in ways leaders may not immediately see.