Standard costs in manufacturing building products are designed to simplify cost management, but they often fail to reflect production reality. As material prices shift, labor conditions change, and product mix evolves, the gap between standard costs and actual costs can grow quickly.

Material prices shift. Labor availability, shift composition, and throughput vary. Run sizes change with demand. Overhead absorbs at rates built on last year’s volume assumptions. None of this appears in the standard cost model until the variance report arrives. By then, pricing decisions, mix decisions, and capacity commitments have already been made.

The gap between what the model says a product costs and what it actually costs to manufacture, deliver, and support is where margin quietly disappears.

For manufacturers serving residential, commercial, and big-box channels, the problem compounds. Different customers consume cost differently, and most margin models fail to reveal it.

Companies that close this gap do more than report better numbers. They make better decisions because the cost model finally reflects the business they actually run.

Get the Executive Brief

This executive brief, “The Cost Accuracy Problem: Why Standard Costs Don’t Reflect Production Reality,” explores the challenges building products finance and operations leaders face when cost models can no longer keep pace with how their plants actually run.

What You’ll Learn

The executive brief examines the cost and margin pressures building products manufacturers are navigating as material volatility, labor complexity, and channel mix create wider gaps between what the cost model shows and what the business is actually earning. It explores why standard costing approaches are struggling to keep pace, including:

- How standard costs drift from reality as material prices and labor conditions change

- How averaged cost models hide margin differences that vary by plant, run size, and throughput

- Why gross margin reporting misses how much customer type and channel affect true contribution

- How overhead allocation methods can obscure which products and plants are actually profitable

Who This Brief is For

We created this brief for finance and operations leaders in building products manufacturing, particularly CFOs, controllers, VP-level finance, and operations directors who are responsible for cost accuracy, pricing decisions, and margin performance across plants and product lines.

A Common Profitability Illusion in Building Products Manufacturing

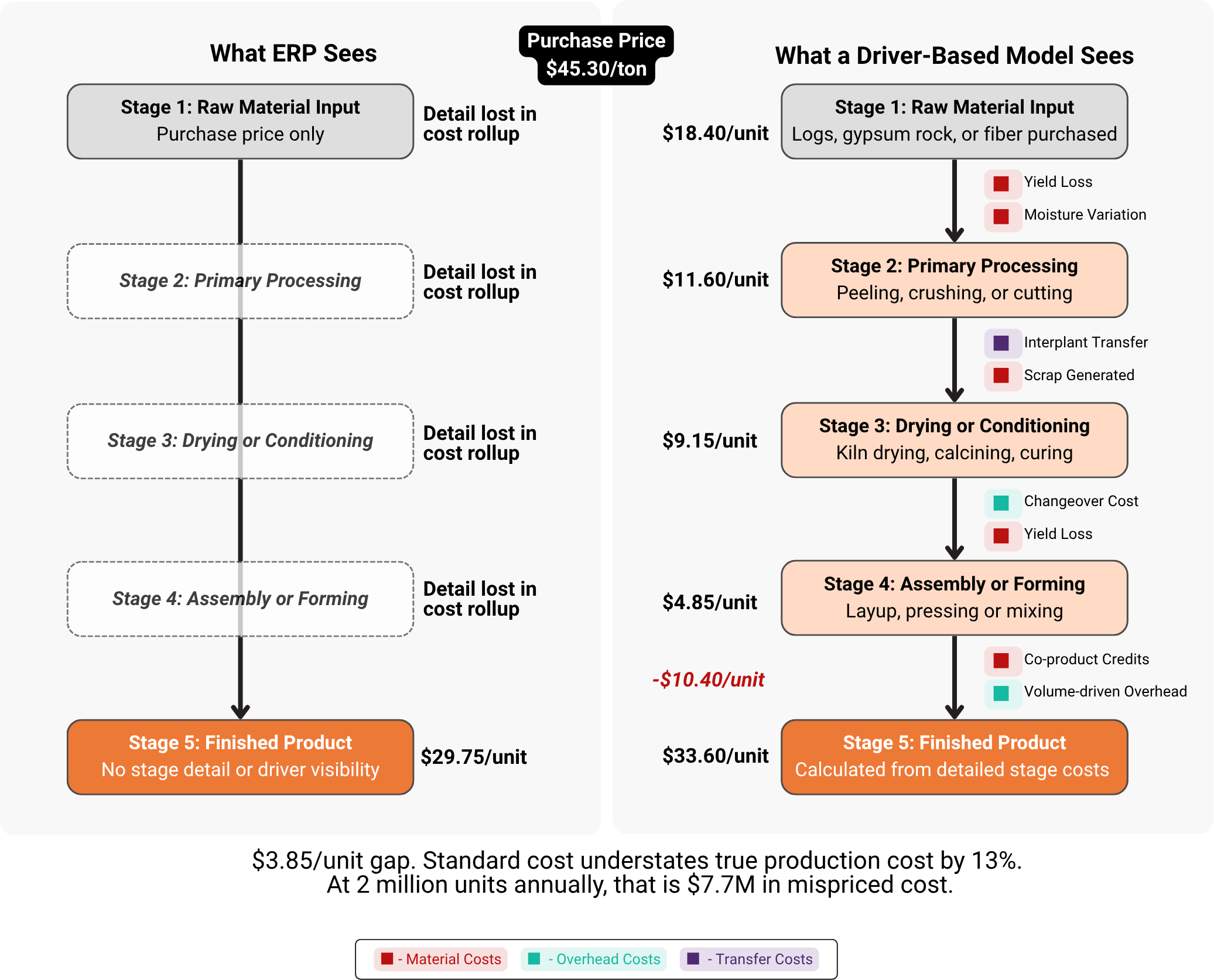

One of the patterns the executive brief explores is how standard cost models create a profitability illusion by collapsing a product’s real cost build into a single number. In building products manufacturing, that number is often built on assumptions that have drifted significantly from how production actually works. Material costs fluctuate by sourcing period and supplier. Yield losses vary by run. Energy costs shift with production method. Labor and overhead layer in differently depending on where and how a product is made. When all of that gets averaged into one standard cost, the model looks clean. But clean and accurate are not the same thing.

How Material Cost Builds Through Production

Plywood is a useful example because the cost story is not simple. Raw timber goes in at one price. What comes out the other end reflects yield loss at peeling, energy consumed during kiln drying, freight if production spans facilities, labor and overhead at press, and co-product credits along the way. By the time a panel is finished, its actual cost per piece is the result of four distinct stages, each adding or offsetting cost in ways a single bundled number cannot show.

This is exactly what a driver-based cost model makes visible. An ERP system sees one material cost. ImpactECS sees every stage, every driver, and every point where cost accumulates or leaks. That distinction matters when material prices move mid-period, when yield rates shift, or when a production decision at one stage affects the economics of every stage that follows.

When manufacturers can trace cost through production rather than just report it at the end, they can answer harder questions: Where is yield loss creating the most cost exposure? Which products are most vulnerable to raw material price swings? Where does a change in production routing actually improve margin?

Three Economic Shifts Reshaping Building Products Margins

The executive brief highlights several shifts in delivery economics that are beginning to reshape profitability across distribution businesses. As freight volatility increases and customer ordering behavior evolves, finance teams are discovering new patterns in how margin is created and where it quietly erodes.

Material Costs Are a Moving Target

Timber, gypsum, cement, and other commodity inputs shift with market conditions that no standard cost reset can fully anticipate. When material prices move mid-period and the cost model doesn’t move with them, every margin calculation downstream is working from the wrong number.

Labor and Throughput Affect Cost More Than Most Models Show

Shift composition, line speed, and run size vary in ways that fixed labor rate assumptions can’t capture. The result is a cost model that reflects a version of the plant that doesn’t exist on any particular day.

Customer and Channel Mix Determine Where Margin Actually Lives

Residential builders, commercial contractors, and big-box retailers each place different demands on production, delivery, and support. When those costs get averaged rather than allocated, the accounts that look most profitable often aren’t.