What CFOs Actually Want from Product Costing and Profitability Analytics

The finance function is under more pressure than ever to deliver answers that drive action. Here is what separates organizations that deliver on that promise from those still working around the limitations of their cost systems.

CFOs today sit at an interesting intersection. Boards and CEOs are asking harder questions about margin, product mix, and profitability by customer and channel. At the same time, the systems most finance organizations rely on for cost data were designed for a different era. They were built around financial reporting, not operational decision-making.

The result is a gap that shows up in budget cycles, pricing conversations, and supply chain decisions. Executives know they have a cost problem. They just don’t always have the right data to act on it.

Conversations across manufacturing, distribution, and process industries point to a clear set of priorities. Finance leaders who are serious about building a cost and profitability analytics capability that delivers real value tend to focus on the same areas.

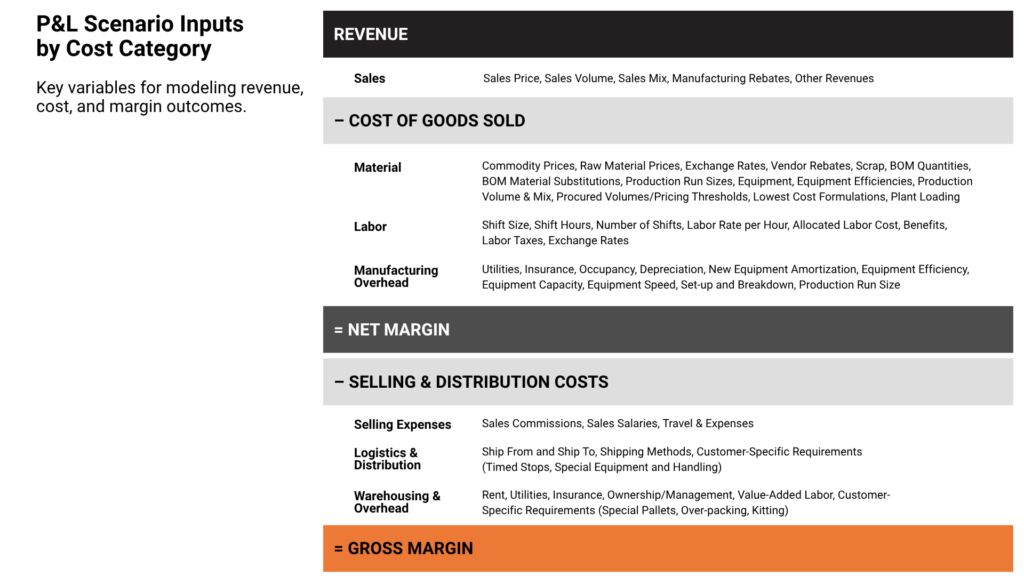

Get the Cost Foundation Right First

Before you can analyze profitability, you need to trust your product costs. That sounds obvious, but it is where most organizations struggle most.

Product cost data in many companies comes from standard cost systems set once and rarely updated. Others rely on spreadsheet models built by individuals who have long since moved on, or overhead allocations that don’t reflect how costs actually behave. When a CFO asks what it actually costs to make a product, the honest answer is often “it depends on which system you look at.”

The solution is advanced cost modeling. These are systems capable of incorporating multiple cost factors: materials, labor, facility and maintenance, production overhead, and post-manufacturing costs. When cost models reflect the real drivers of cost rather than simplified assumptions, they become a foundation for every downstream analysis. Pricing, margin analysis, quoting, and scenario planning all get better when the underlying cost data is accurate.

CFOs who have made progress here share a common approach. They stop treating cost accuracy as a finance problem to solve in isolation. They treat it as a shared data problem involving operations, supply chain, and IT. Product costs are a function of bills of materials, routings, machine rates, labor rates, and inbound logistics costs. Getting those inputs right requires connecting data across systems and establishing shared governance around how that data is maintained.

Link Costs to Their Drivers

Accurate costs are necessary. Understanding why costs behave the way they do is what makes those costs actionable.

Driver-based costing links costs directly to the operational activities that cause them. It replaces simplified allocation methods with a more accurate picture of how different factors affect total costs. This enables more precise assignment of costs to specific products, services, customers, or business units.

The practical value is substantial. When costs are traced to their drivers, cost control becomes more specific. Instead of knowing that overhead is too high, finance leaders can see which activities are driving that overhead and where operational changes would have the most impact. Budgeting and planning become more accurate because cost assumptions reflect how the business actually operates today, not how it operated when the allocation rates were last set.

Driver-based costing also helps identify where investment makes sense. Visible cost drivers allow CFOs to evaluate which operational improvements or capital investments will produce the most meaningful reduction in unit costs or improvement in margins.

Build Scenario Modeling Into How Finance Operates

The business environment has become more volatile. Tariff changes, raw material price swings, currency fluctuations, and supply chain disruptions can all shift product economics significantly. Finance organizations that can model the impact of those changes quickly are better positioned to support leadership decisions in real time.

Scenario analysis is not a new idea in finance. What has changed is the expectation around speed and specificity. A CFO who needs to understand the margin impact of a commodity price increase or a major volume shift shouldn’t have to wait two weeks for the analysis. That analysis should be available in hours, or ideally minutes. And it shouldn’t require rebuilding the model from scratch each time.

That level of responsiveness requires a maintained cost model. It must connect to current cost data and be structured to answer the questions leaders actually ask. The most common scenario types include raw material and commodity price sensitivity, volume and product mix changes, new product cost estimation, make-vs.-buy analysis, foreign exchange rate changes, and supply chain network decisions.

Each of these requires a model that reflects the full cost structure of the business. When that infrastructure exists, the finance team becomes the group that can answer hard questions quickly. That changes how finance is perceived across the organization.

Understand the True Cost of Serving Customers

Product profitability at the gross margin level is a starting point, not an endpoint. The CFOs who get the most value from their analytics have moved well beyond standard margin reporting.

Cost-to-serve analysis builds a fully loaded view of what it costs to serve specific customers, channels, or markets. It includes outbound logistics, warehousing, customer-specific rebates and incentives, returns, and the cost of sales and service. These post-manufacturing costs can be substantial. They also vary significantly by customer and channel.

When those costs are layered into a complete product and customer P&L, the picture often looks very different from what the standard margin report shows. Products that appear profitable on a gross margin basis may be destroying value once full cost-to-serve is included. Customers that appear to be strong revenue contributors may generate far less value than smaller accounts with lower service complexity.

This kind of analysis changes conversations across the business. Pricing decisions, customer negotiations, product portfolio reviews, and channel strategy all improve when grounded in a complete picture of cost and profitability.

Getting there requires two things: clean cost data at the product level, and the ability to assign post-manufacturing costs in a way that reflects actual consumption. Revenue-based allocations rarely tell the real story.

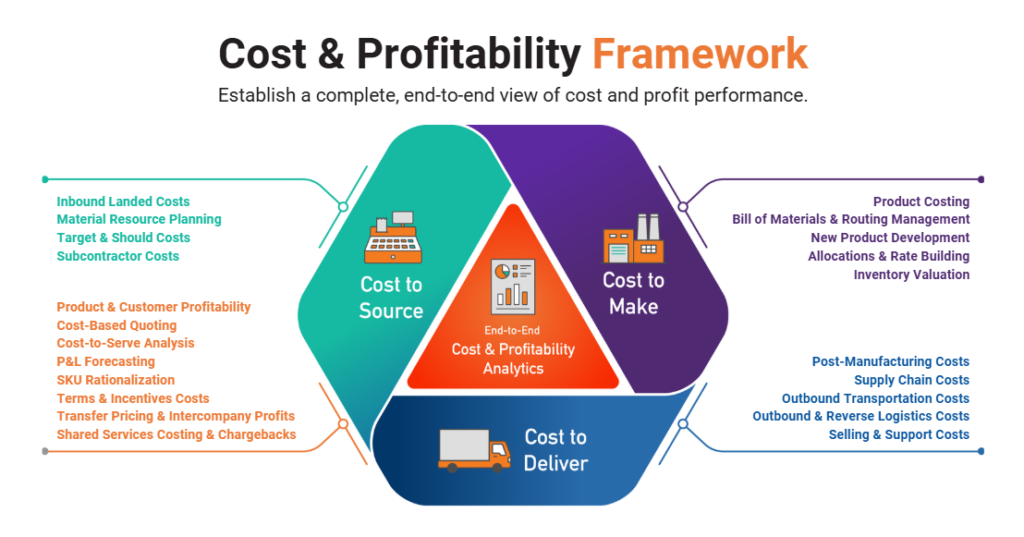

Build an Integrated View Across the Full Value Chain

One of the most common limitations in cost and profitability analytics is that the analysis stops at the plant gate. Manufacturing cost gets detailed attention. Inbound procurement costs, supply chain costs, outbound logistics, and customer-specific costs get handled with approximations.

This is partly a legacy of how cost systems evolved. Manufacturing cost systems were built to calculate standard costs for inventory valuation. Extending that analysis across the full value chain was never part of the original design.

But for most CFOs trying to understand product and customer profitability, that limitation is a serious constraint. The most important cost differences between products often lie not in manufacturing but in what it costs to source materials, deliver finished goods, and serve customers. Ignoring those costs means making decisions on incomplete information.

An integrated profitability view combines data from procurement and supplier systems, manufacturing execution systems, warehouse and logistics systems, and customer-facing systems. It creates the ability to track and simulate financial performance across every stage of the value chain, identify the true drivers of cost and profit, and evaluate the cost-effectiveness of different strategies.

Organizations that have built this view consistently describe meaningful shifts in their strategic priorities. Sourcing decisions that seemed straightforward look different when inbound landed costs are properly accounted for. Products that seemed equivalent on manufacturing cost look very different at the fully loaded level.

Foster Collaboration Around Cost Data

Technology and data are necessary but not sufficient. The organizations that get the most value from their cost and profitability capabilities have built something that goes beyond systems: a shared commitment to understanding and managing cost across the business.

Sharing cost information across functions creates a shared understanding of the financial implications of decisions. When operations leaders understand the cost impact of their choices, when product managers think about margin when adding SKUs, and when sales teams understand the profitability of the deals they structure, finance doesn’t have to catch every problem after the fact.

This kind of cost culture doesn’t happen automatically. It requires finance leaders who share cost data broadly and build tools that make cost information accessible to non-finance audiences. It also means reinforcing the connection between operational decisions and financial outcomes. Collaboration surfaces insights that finance alone would miss. Sales teams understand customer behavior. Operations teams understand production variability. Both improve cost models when that knowledge is incorporated.

CFOs who have built this environment describe it as one of the highest-leverage investments they have made in the function.

Make Technology Work for the Business, Not Just for Finance

Technology plays a critical role in making all of this possible. Advanced analytics platforms handle large volumes of data, perform complex cost calculations and modeling, and integrate with ERP and operational systems. They allow finance teams to work at a scale and speed that spreadsheets cannot match.

The right technology reduces manual effort, limits errors, and frees the finance team to spend time on analysis rather than data assembly. It also makes it practical to maintain the cost models and scenario capabilities described above, without requiring a complete rebuild each quarter.

AI and machine learning capabilities are adding meaningful value as they mature. Pattern recognition across large cost datasets, anomaly detection in product costs, and natural language interfaces allow business users to query cost and profitability data without needing to understand the underlying model. These capabilities are most valuable when they sit on top of clean, well-structured cost data. The quality of the foundation determines the quality of the output.

CFOs evaluating technology for cost and profitability analytics should prioritize three things: scalability, flexibility to accommodate the organization’s specific cost structure, and integration depth with existing systems.

The Capability Gap Is Real, but Closable

For many finance organizations, a significant gap exists between the cost and profitability analytics capability they have today and the one they need to answer the questions that matter most.

Closing that gap is not primarily a technology problem. It is a combination of data quality, process discipline, organizational alignment, and the right analytical framework. Technology accelerates the work, but the foundation has to be built deliberately.

Finance leaders who have invested in building this capability describe it as one of the highest-return investments they have made in the function. Answering hard questions quickly, with data people trust, changes how finance is perceived and how it contributes to the business.

That capability doesn’t happen by accident. It starts with a clear view of where the gaps are and a commitment to closing them systematically.

About 3C Software

3C Software helps finance and operations teams understand costs, analyze profitability, and make better decisions across the business. Its ImpactECS platform connects data across systems, models how costs behave, and turns complex cost structures into clear, actionable insight. Companies use ImpactECS to analyze profitability by product, customer, and channel, uncover cost drivers across the value chain, and evaluate scenarios with confidence. The result: finance and operations leaders who can stop guessing and start acting on numbers they trust.